You have probably heard that homeowners today have a lot of equity. But that phrase gets repeated so often it starts to lose its weight. What does it actually mean, how much are we talking about in real dollars, and what can you actually do with it?

This piece answers all three questions and walks through four concrete ways to put that equity to work based on where you are in life right now.

What Is Home Equity and How Does It Build?

Home equity is the portion of your home’s value that you own outright, free of any mortgage balance. It builds in two ways: as you pay down your loan principal over time, and as your home’s market value increases. The formula is simple, current market value minus what you still owe equals your equity.

In a market like Middle Tennessee, where home values across Franklin, Brentwood, and the surrounding communities have appreciated significantly over the past decade, most homeowners have been building equity on both fronts simultaneously.

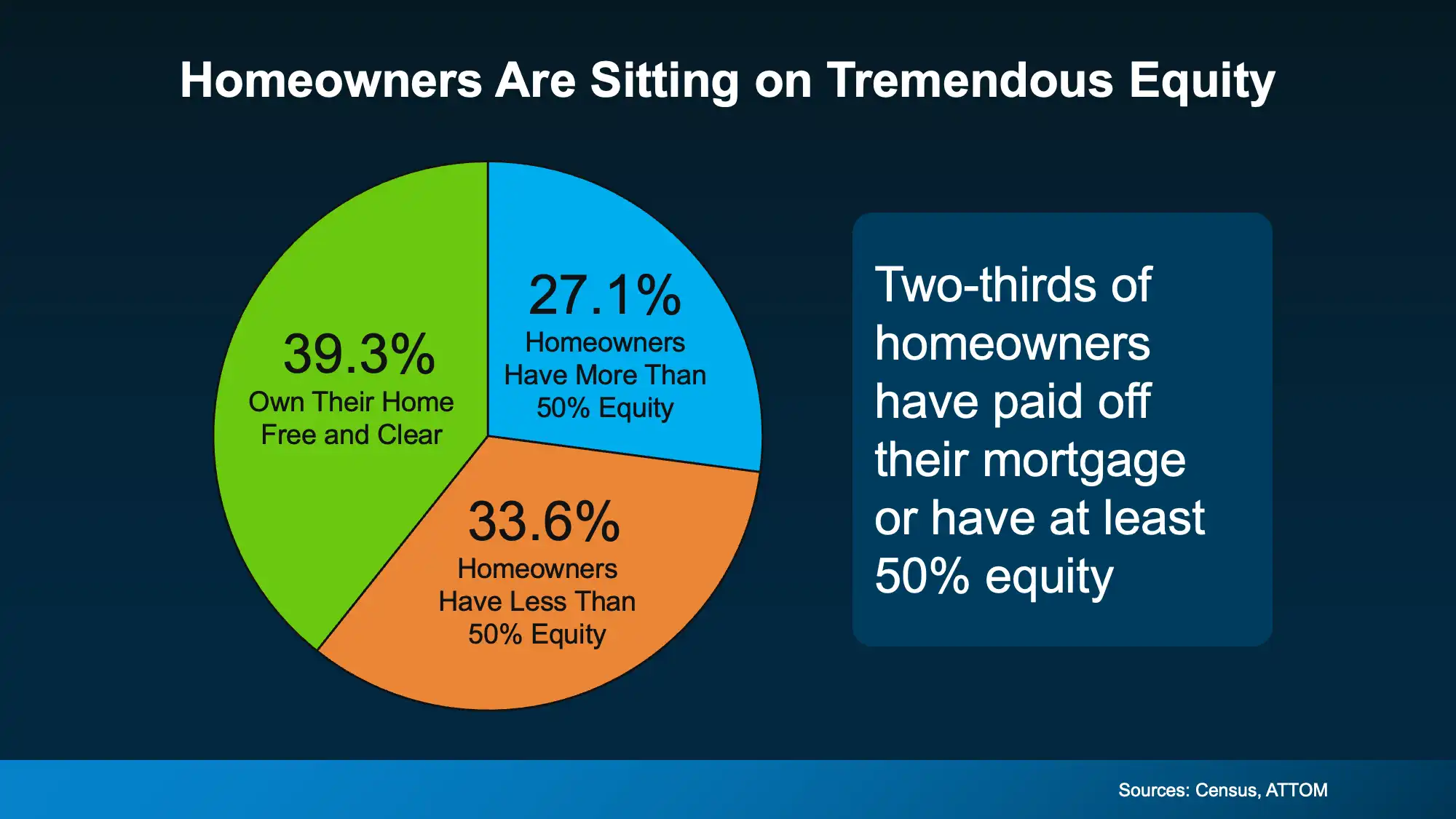

How Much Equity Does the Typical Homeowner Have Right Now?

According to data from the U.S. Census Bureau and ATTOM, roughly two-thirds of American homeowners currently hold a substantial equity position. Specifically, 39 percent own their homes outright with no mortgage balance remaining, and another 27 percent have at least 50 percent equity in their properties.

In real dollar terms, Cotality estimates the typical homeowner holds close to $300,000 in equity today. That is a significant financial asset, and for many households, it is the single largest one they have.

Understanding where you stand personally is the starting point for any of the strategies below. If you are not sure what your home is worth in the current market, our home value tool is a quick way to establish a baseline.

The market heading into 2026 continues to support strong equity positions across Middle Tennessee, which makes this a particularly timely conversation.

Four Ways to Use Your Home Equity Strategically

| 1. Move Into a Home That Better Fits Your Life Today |

Your equity can serve as a down payment on a home that is a better match for where you are now. Maybe the house felt right a decade ago and no longer does. Families grow. Children move out. Remote work changes how you use space. Health and mobility considerations shift what you need in a floor plan.

Depending on how much equity you have accumulated, you may be in a position to purchase your next home with significantly less debt than you carried previously, or in some cases, none at all. If you are thinking about making a move, browsing what is currently available is a useful way to calibrate expectations. And if new construction is on your radar, there is a compelling case for it right now, as we covered in our piece on why this may be the best time to buy a brand-new home in Nashville.

| 2. Reinvest in Your Current Property |

If you are not ready to move, equity can fund improvements to the home you already own. Kitchen renovations, updated bathrooms, and energy efficiency upgrades tend to perform well at resale — but the return on any given project depends heavily on your specific neighborhood and price point.

Before committing to a project list, talking with a real estate advisor who knows your market well is the most efficient way to prioritize. What adds value in Franklin may not track the same way in East Nashville or Nolensville.

| 3. Fund a Major Life Goal |

Home equity is not limited to real estate decisions. Many homeowners use it to fund goals that have nothing to do with property at all, starting or expanding a business, contributing to retirement, covering education costs, or helping a family member with a down payment of their own.

That last use case is particularly relevant in a market where home prices have made entry-level ownership more challenging for younger buyers. If you are thinking about helping someone you love get into a home, your equity may already be the resource that makes it possible. Our buyer resources can help them understand what the purchase process looks like from their side of the table.

| 4. Create a Financial Safety Net During Hardship |

Equity is also a lifeline when circumstances become difficult. Homeowners who fall behind on payments often have more options than they realize. If you have meaningful equity and find yourself unable to sustain your mortgage, selling and walking away with those funds is frequently a far better outcome than foreclosure — both financially and for your credit.

If that is a situation you are managing, it is worth understanding what your options look like when a sale does not go as planned, and then having a direct, confidential conversation with an advisor before the timeline gets constrained. The factors that influence how quickly and cleanly a home sells are worth understanding before you commit to a path.

How Much of Your Equity Is Actually Accessible?

Not all equity is immediately spendable, but most homeowners have more accessible equity than they assume. The key metric here is tappable equity: the portion you can access through a cash-out refinance or home equity line of credit while still maintaining a 20 percent equity cushion in the property.

That 20 percent threshold matters. It is the standard buffer most lenders require and the guardrail that protects homeowners from becoming overleveraged, a lesson the 2008 housing crisis made painfully clear. Maintaining that cushion keeps your loan-to-value ratio healthy and preserves your financial flexibility if values fluctuate.

According to the Intercontinental Exchange, as of Q4, U.S. mortgage holders collectively hold $17.3 trillion in home equity. Of that, $11.2 trillion qualifies as tappable equity, accessible while still maintaining that 20 percent threshold. The vast majority of today’s homeowners have meaningful room to work with.

| $11.2 Trillion Total tappable equity available to U.S. mortgage holders while maintaining a 20% equity cushion. Source: Intercontinental Exchange, Q4 2025. |

For a broader look at how these market conditions are shaping up locally, our overview of navigating Nashville’s real estate market covers the dynamics directly relevant to Middle Tennessee homeowners.

What Should You Do Next?

Step 1: Establish your current equity position. Our home value tool gives you a starting estimate, and from there our team can provide a more detailed, market-specific assessment for your property.

Step 2: Match your equity to your goal. If you are considering a move, our seller resources walk through how that process works. If your goal is financial — retirement, a business, a family loan — bring in a financial advisor alongside your real estate conversation so you are weighing both the real estate and tax implications together.

Home equity is one of the most significant financial assets many people hold. In a market where values have held strong, it represents real flexibility and real momentum. Whether you are thinking about a move, a renovation, a life goal, or simply want to understand where you stand, knowing your number is the right place to start.

What is one goal you would go after right now, if you had the resources for it? We would be glad to help you figure out whether your equity gets you there.

Frequently Asked Questions About Home Equity

What is the average home equity in the U.S. right now?

According to Cotality, the typical American homeowner holds close to $300,000 in equity as of 2025. This figure varies based on local market appreciation, how long the homeowner has owned the property, and how much of the mortgage has been paid down.

How do I access my home equity?

The three most common methods are a cash-out refinance, a home equity line of credit (HELOC), or a home equity loan. Each carries different interest rates, terms, and tax implications. Consulting both a financial advisor and a real estate professional before choosing a method is advisable.

How much equity should I keep in my home?

Most financial advisors and lenders recommend maintaining at least 20 percent equity in your home at all times. This protects your loan-to-value ratio, satisfies most lender requirements, and provides a financial cushion if market values decline.

Can I use home equity to help a family member buy a home?

Yes. Some homeowners use a cash-out refinance or HELOC to access equity and then gift or loan those funds to a family member for a down payment. This is a common strategy in markets where entry-level home prices have risen significantly. Tax rules around gift giving apply, so consulting a financial advisor beforehand is recommended.

What is tappable home equity?

Tappable equity is the portion of your home equity that can be accessed through a cash-out refinance or home equity line of credit while still maintaining a 20 percent equity stake in the property. As of Q4 2025, U.S. homeowners hold a combined $11.2 trillion in tappable equity, according to the Intercontinental Exchange.

Is using home equity a good idea if I am struggling financially?

If you have meaningful equity and are facing financial hardship, selling your home may be a better option than foreclosure. Homeowners who sell proactively can walk away with their equity intact rather than losing both the home and their financial standing. Speaking with a real estate advisor early gives you the most options.

More Blogs You Might Find Interesting

– It’s Getting More Affordable To Buy a Home

– Your Home Didn’t Sell? What to Do.

– Why Some Homes Sell Quickly and Others Don’t Sell at All

Social Cookies

Social Cookies are used to enable you to share pages and content you find interesting throughout the website through third-party social networking or other websites (including, potentially for advertising purposes related to social networking).