For a lot of parents and grandparents, watching a family member struggle to buy their first home right now is hard. You saw firsthand how homeownership gave your life stability and helped grow your net worth. You want those same opportunities for the people you love.

With all the affordability challenges in recent years, that can feel like an uphill battle. But here’s what you may not have considered: if you’ve owned your home for any meaningful stretch of time in this market, you may already be sitting on the tool that changes everything for them.

Home equity in Middle Tennessee has grown substantially over the past decade. That equity doesn’t have to stay locked in your walls until you sell or retire. For many homeowners, it’s become the most direct way to give the next generation a real shot at ownership.

What Does Equity Have to Do With Someone Else Buying a Home?

Equity is the difference between what your home is worth and what you still owe on it. If your home has appreciated, or you’ve paid down your mortgage over the years (or both), the gap between those two numbers can be significant. According to Cotality, the typical American homeowner holds close to $300,000 in tappable equity today.

That number is higher in markets like Belle Meade, Green Hills, Brentwood, and Franklin, where appreciation has outpaced national averages for years. Homeowners in these zip codes who purchased even five to seven years ago have often seen their equity grow beyond what they ever projected. A portion of that equity can be accessed through a home equity line of credit or a cash-out refinance and gifted or loaned to a family member for a down payment.

This is not a niche strategy.

It is increasingly how first-time buyers in expensive markets are finally getting into homes.

What Is Actually Stopping Young Buyers Right Now?

It’s easy to assume that mortgage rates or high prices are the primary obstacle for first-time buyers. Those are real factors. But when John Burns Research and Consulting surveyed renters about what was keeping them from purchasing, the number one answer was the upfront cost: specifically, not having enough saved for a down payment.

Rates can come down. Prices adjust over time. But accumulating $60,000 to $100,000 in cash for a down payment on a home in Nashville’s more established neighborhoods, while also paying rent and managing everyday expenses, is a math problem that doesn’t resolve quickly on its own.

That’s the specific gap where a homeowner with significant equity can actually move the needle. You can’t control rates. You can’t set prices. But you may be able to close the one obstacle that is concretely in the way.

How Are Families Actually Using Equity to Help With Down Payments?

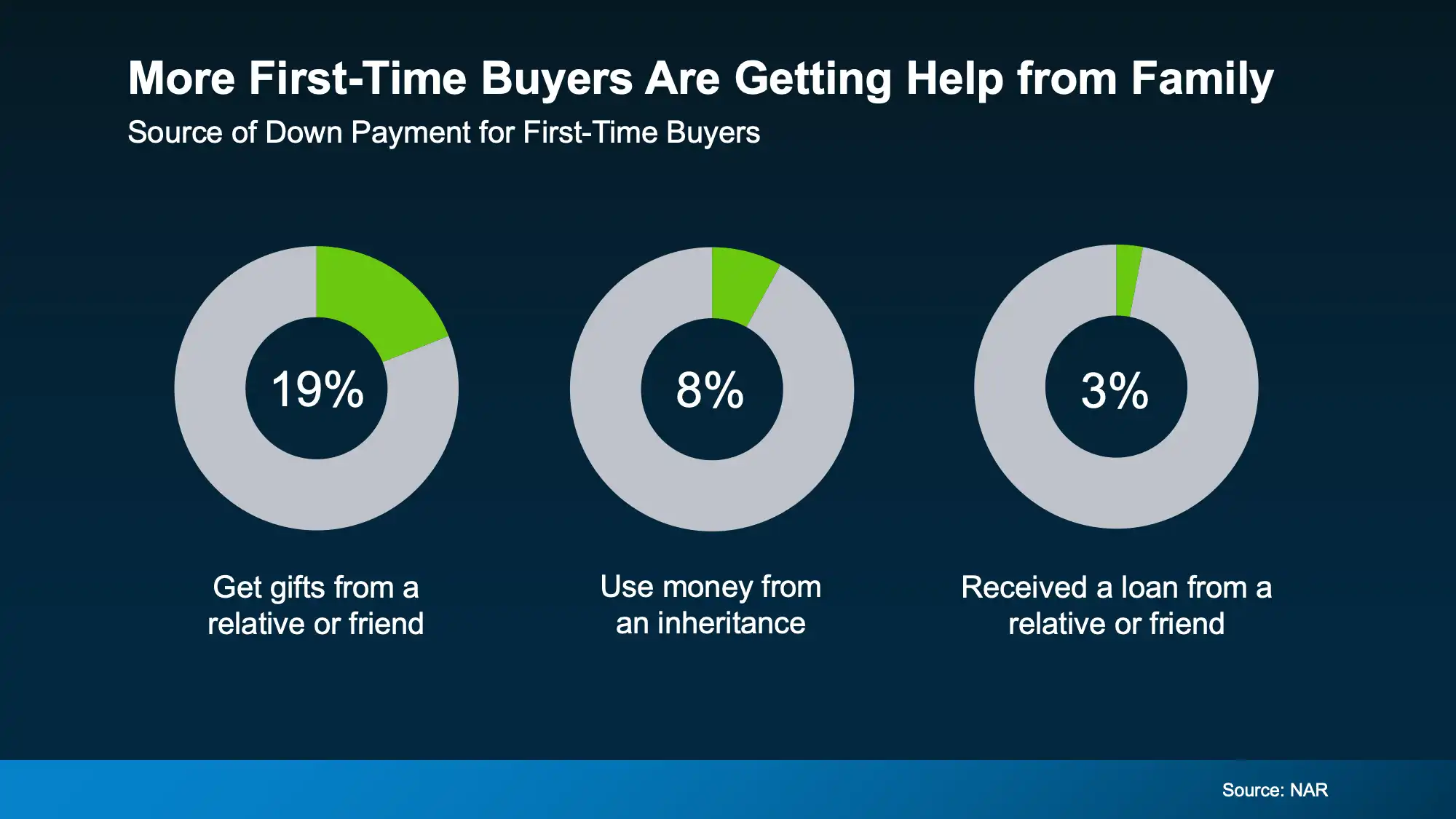

Family financial support for down payments is not rare. According to the National Association of Realtors, nearly 1 in 5 first-time buyers use a cash gift from family or a loved one to fund part of their down payment. Additional buyers use inheritance funds or informal loans from someone they know to bridge the gap.

The mechanisms most commonly used by homeowners looking to help family members include:

- A direct cash gift drawn from a home equity line of credit (HELOC), which allows access to equity without selling the home.

- A cash-out refinance that converts a portion of equity to liquid funds, which are then gifted or loaned to the buyer.

- A structured family loan at below-market rates, documented to satisfy lender requirements.

- Early inheritance distribution, which some families are choosing deliberately rather than waiting until the estate is settled.

Each option has different tax and lending implications. A mortgage professional and a financial advisor should be part of the conversation before anything is finalized.

Does Helping a Family Member Mean Risking Your Own Financial Future?

This is the question most homeowners think about first, and it is the right one to ask. Giving away equity is not without consequences. But for many homeowners, the math is more forgiving than they expect.

Consider a homeowner who purchased in Belle Meade or Brentwood years ago and has seen their home appreciate significantly. Their equity may have grown well beyond what they need for retirement or a future purchase. Giving $80,000 to $100,000 to help a child or grandchild with a down payment, while keeping the majority of their equity intact, is a realistic option for many. The key is understanding exactly what your current home is worth before making any commitments.

This is also part of a broader pattern. An estimated $68 trillion to $84 trillion in wealth is expected to transfer from older generations to younger ones over the next two decades, according to Cerulli Associates. Many families are no longer waiting. They are choosing to pass wealth down while they can see it put to use.

What Happens After the Down Payment: Why This Gift Has Long-Term Impact

A down payment gift isn’t just a transaction. It is the starting point for a family member’s equity-building story. Once they are in a home, their net worth starts growing in the same way yours did. They stop paying rent and start accumulating ownership.

In a market where timing and entry price shape long-term outcomes more than almost any other variable, getting into a home now rather than waiting several more years can represent a meaningful difference in future wealth. Younger buyers who can get in sooner rather than later are better positioned, regardless of where rates go in the near term.

Is This the Right Move for Your Situation?

The first step is knowing where you stand. Getting a current picture of what your home is worth is the foundation for any equity decision, whether you are thinking about a gift, a refinance, or eventually a sale that funds the next chapter for your whole family.

If a sale is part of the plan, understanding how the process works from a seller’s perspective, including what preparation looks like and how to time the transaction, is also part of the equation. The seller resources and process guidance on this site are built for homeowners navigating exactly these kinds of decisions.

Frequently Asked Questions About Using Home Equity to Help Family Buy a Home

What is tappable home equity and how much do most homeowners have?

Tappable equity is the portion of your home’s value you can access without selling, typically through a HELOC or cash-out refinance. According to Cotality, the typical American homeowner holds close to $300,000 in tappable equity as of 2025. In higher-value markets like Brentwood, Belle Meade, and Green Hills, that figure is often significantly higher.

Can I give my child money from my home equity for a down payment?

Yes. Many homeowners access equity through a HELOC or cash-out refinance and gift the proceeds to a family member for a down payment. Mortgage lenders typically require a gift letter documenting that the funds are not a loan. There are also annual gift tax exclusion limits to be aware of, so consulting a tax advisor before proceeding is a good idea.

How many first-time buyers use family gifts for their down payment?

According to the National Association of Realtors, nearly 1 in 5 first-time buyers use a cash gift from family or a loved one to help fund their down payment. Additional buyers rely on informal family loans or early inheritance distributions. Family financial support has become one of the most common ways buyers clear the upfront cost barrier in expensive markets.

Is gifting home equity to a family member risky for my retirement?

It depends on your total equity position and retirement plan. For many homeowners in Middle Tennessee who purchased years ago and have seen significant appreciation, gifting a portion of equity does not meaningfully threaten their financial security. Getting an accurate home valuation first is the essential starting point before committing to anything.

What is the biggest obstacle preventing first-time buyers from purchasing a home?

According to John Burns Research and Consulting, the number one barrier for renters who want to buy is the upfront cost, particularly saving enough for a down payment. Mortgage rates and home prices, while real concerns, ranked lower in surveys. This makes down payment assistance from family one of the most targeted ways to remove the primary obstacle.

How does an early inheritance or family gift affect a first-time buyer’s mortgage application?

Lenders will ask for documentation of any large deposits in a buyer’s bank account, including down payment gifts. A formal gift letter stating the funds are a gift and not a loan is standard. If the transfer is structured as a family loan rather than a gift, the lender will factor in the monthly payment obligation when calculating the buyer’s debt-to-income ratio.

What is the first step for a Middle Tennessee homeowner thinking about helping a family member with a down payment?

The most important first step is understanding exactly what your home is worth today and how much equity you have. From there, a conversation with a mortgage professional and a financial advisor can clarify which access mechanism (HELOC, cash-out refinance, or direct gift) makes the most sense for your situation.

How does helping a younger family member buy a home benefit them long term?

Once a buyer is in a home, they stop paying rent and begin building equity. In a market like Middle Tennessee, where home values have appreciated consistently over time, getting into a home sooner rather than later has historically produced meaningful long-term wealth. A down payment gift accelerates the timeline and can have compounding financial benefits for the recipient over the following decades.

Bottom Line

If you are curious what your home equity could make possible, for you or for someone you love, start with a simple conversation. Because sometimes the most meaningful investment you can make is for the next generation.

Reach out to schedule a no-pressure conversation about your options in Middle Tennessee.

Social Cookies

Social Cookies are used to enable you to share pages and content you find interesting throughout the website through third-party social networking or other websites (including, potentially for advertising purposes related to social networking).